Content Summary

Access this content

Choose an option below

Your content has been opened.

Register to access this content

Verify your email to access this content

Code sent. Enter it in the modal

Your content has been opened.

Why do I need to verify I’m human?

Please verify you are a human before opening this content.

Your content has been opened.

The content will open in a new window. You may need to allow popups for this site.

Check your inbox

Oil & Gas in 2026: When Volatility Enters, Working Capital Is Your Best Defense has been emailed to . Entered the wrong email?

Don't see the content in your inbox?

Make sure to check your spam and other messages folders.

Can't get to your email right now?

By accessing content on the AFP Treasury and Finance Marketplace you agree to our Terms of Service and Privacy Policy; and, you acknowledge that your information may be shared with the content publisher.

You might also be interested in

The CFO's H2 Working Capital Agenda: 4 Decisions to Make Now

H2 planning tends to generate more noise than signal: cascading scenarios, overlapping dashboards, and an endless queue of initiatives that each claim to be quick wins. What most...

Read More

Your Supply Chain Is Only as Strong as Your Suppliers' Cash Flow

Extended payment terms may improve your working capital on paper, but they can quietly increase risk across your supply base. This article explains the hidden cost of supplier...

Read More

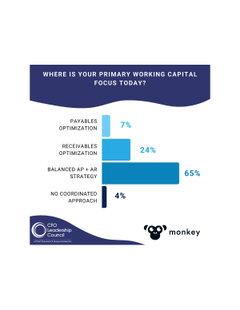

CFOs Want a Balanced Working Capital Strategy. 65% of CFOs Want a Balanced Working Capital Strategy. Most Don't Have the Infrastructure to Pull It Off.

In a survey conducted with the CFO Leadership Council to explore working capital priorities, 65% of respondents said their top priority is balancing AP and AR strategies.

Read More